Thank you for completing the Savings Quiz! Below are the assumptions and methodologies that ComposedPro uses to calculate your savings.

The assumptions described below that are used in the Savings Quiz may not be accurate for your unique situation. The results of the savings quiz are for informational purposes only. The projected savings or other information generated by the Savings Quiz will not match actual results and are not a guarantee of any current or future savings.

The Savings Quiz is information and designed to show you two things:

- the possible ways you might be able to save by using ComposedPro.

- how we think about portfolio management. ComposedPro is primarily focused on helping you in areas that you CAN control (fees and taxes), and worried less about areas you cannot control.

The five areas below are what ComposedPro focuses on to lower fees and taxes in your portfolio:

- Investment Expense Savings

- Advisor Expense Savings

- Match Savings

- Contribution Placement Savings

- Investment Placement Savings

OVERALL ASSUMPTIONS

All savings are calculated using the basic formula:

Savings =

(Total Retirement Withdrawals + Ending Portfolio Balance Using ComposedPro)

MINUS

(Total Retirement Withdrawals + Ending Portfolio Balance Not Using ComposedPro)

Retirement Assumption - We assume everyone will retire at 67. Starting that year we assume an after-tax withdrawal need of 4% of the portfolio. This is calculated as:

4% from tax-exempt funds (no after-tax conversion needed) plus 4% tax-deferred funds (converted to after-tax) plus 4% from taxable portfolio (converted to after-tax).

THIS IS NOT A RECOMMENDED WITHDRAWAL RATE, BUT MERELY AN ASSUMPTION FOR THE SAVINGS QUIZ. There are many reasons why a 4% withdrawal rate might not be suitable for your unique situation. We assume you continue to make withdrawals through the year you are age 95. We then take note of the total withdrawals in retirement and the ending portfolio balance.

Income Assumptions - if you and your spouse work at an employer and are under our retirement age assumption, we assume you earn the following in pre-tax income in today's dollars

- $50,000 at age 21

- $70,000 at age 30

- 100,000 at age 40 and beyond

If you answered N/A (that you did not work at an employer), then we assume $0. If you indicate that you married and the sole earner in your household, we assume you earn 1.5x the income assumptions above, and your spouse earns $0. We inflate the income assumptions in each projected year of the Savings Quiz.

Income Tax Rate Assumptions - We assume you reside in the state which would produce the highest state income tax rate based on the income assumptions above. Your ordinary income tax rate is the state income tax rate plus the federal income tax rate using the appropriate brackets related to our income assumptions above. Your capital gains tax rate is the state income tax rate plus the federal capital gains rate using the appropriate brackets relating to our income assumptions above.

Employer Match - we assume a match rate of 50% of the employee contribution with a max employer match of 3%.

Investment Return Assumption - we allocate your portfolio on a glide path across the different asset categories used by ComposedPro. This glide path gets more conservative over time. Please see ComposedPro's Investment Methodology for more information. Within that article, you can see our current risk and return assumptions for each asset category. The Savings Quiz uses a weighted average of these return assumptions to determine the investment returns within each of your Tax-Exempt, Tax-Deferred, and Taxable accounts.

Tax-Exempt Portfolio Return Assumption = weighted average of the asset category returns within your tax-exempt portfolio minus an advisor fee

Tax-Deferred Portfolio Return Assumption = weighted average of the asset category returns within your tax-deferred portfolio minus an advisor fee minus employer investment fees (see Investment Expense Savings later)

Taxable Portfolio Return Assumption = weighted average of the asset category returns within your taxable portfolio minus an advisor fee

SAVINGS ASSUMPTIONS

1. Investment Expense Savings - these are expense savings you may realize by lowering the behind-the-scenes fees on your investments. Many investments such as mutual funds and ETFs have expense ratios, which reduce the value of your investment over time.

- If you or your spouse, if applicable, work at a larger employer, we assume the employer investment fees in your Tax-Deferred accounts without ComposedPro are 0.40%, and that using ComposedPro could lower these fees to 0.20% by choosing better investment options within your employer plans.

- If you or your spouse, if applicable, work at a smaller employer, we assume the employer investment fees in your Tax-Deferred accounts without ComposedPro are 0.80%, and that using ComposedPro could lower these fees to 0.40% by choosing better investment options within your employer plans.

- If you work at a larger employer and your spouse works at a smaller employer, or vice versa, we assume the employer investment fees in your Tax-Deferred accounts without ComposedPro are 0.60%, and that using ComposedPro could lower these fees to 0.30% by choosing better investment options within your employer plans.

We determined these savings by grouping our clients who had employer-sponsored retirement plans ("ESRAs") into plans at large (more than 10,000 employees) and smaller employers. We documented their plan allocations prior to receiving our advice and compared it to our recommendations. Our average saving on larger plans was over 0.30%, and for clients with ESRAs as smaller employers it was over 0.40% in savings within the ESRA account.

2. Advisor Expense Savings - these are expense savings you may realize depending on the fees charged by your advisor, if applicable. The ComposedPro advisor fee is the AUM fee on ComposedPro's highest service level.

- If you currently have a traditional advisor, we assume that the advisor costs you 1.0% annually on assets under management (AUM). You would realize savings in this scenario based on the difference between 1.0% and ComposedPro's AUM fee and subscription fee.

- If you currently have a robo advisor, we assume that the advisor charges the same AUM fee as ComposedPro but we add in ComposedPro's subscription fee. This subscription fee would be an added cost on your portfolio.

- If you do not currently have an advisor, then we not only assume no savings are possible and that ComposedPro's AUM and subscription fees will be an added cost on your portfolio.

3. Match Savings - these are savings you may realize by allocating your contributions properly in order to get the full benefit of the employer match within your employer-sponsored retirement plan.

- If you indicate you currently contribute enough to a retirement plan to receive the full employer match, then we assume no savings. Specifically, we assume you contribute 1.0% of your gross income to tax-exempt, 5.0% to tax-deferred, and 6.0% to taxable accounts from your pre-tax income.

- If you indicate you do contribute to a retirement plan where you work, but not enough to receive the full employer match, then we assume you are missing out on 2.4% of your max 3.0% employer match. Specifically, we assume you contribute 0.2% of your gross income to tax-exempt, 1.0% to tax-deferred, and 6.0% to taxable accounts from your pre-tax income. Savings are generated by moving a portion of your taxable contribution to tax-deferred and tax-exempt in order to receive the full company match. Any amounts moved from taxable to tax-deferred are adjusted to be after-tax equivalent.

- If you indicate you do not know if you contribute enough to a retirement plan to receive the full employer match, then we assume you are missing out on 2.4% of your max 3.0% employer match. Specifically, we assume you contribute 0.2% of your gross income to tax-exempt, 1.0% to tax-deferred, and 6.0% to taxable accounts from your pre-tax income. Savings are generated by moving a portion of your taxable contribution to tax-deferred and tax-exempt in order to receive the full company match. Savings are generated by moving a portion of your taxable contribution to tax-deferred and tax-exempt in order to receive the full company match. Any amounts moved from taxable to tax-deferred are adjusted to be after-tax equivalent.

- If you indicate you do not contribute anything to a retirement plan, then we assume you are missing out on the full 3.0% of the max 3.0% employer match. Specifically, we assume you contribute 0.0% of your gross income to tax-exempt, 0.0% to tax-deferred, and 6.0% to taxable accounts from your pre-tax income. Savings are generated by moving a portion of your taxable contribution to tax-deferred and tax-exempt in order to receive the full company match. Any amounts moved from taxable to tax-deferred are adjusted to be after-tax equivalent.

- If you indicate that your employer does not have a retirement plan that you can contribute to, then we assume you do not any opportunity for a company match. However, we do assume that you contribute to accounts outside your employer. Specifically, we assume you contribute 1.0% of your gross income to tax-exempt, 5.0% to tax-deferred, and 6.0% to taxable accounts from your pre-tax income.

4. Contribution Placement Savings - these are income tax savings you may realize by maintaining minimum balances in your tax-exempt, tax-deferred, and taxable accounts. There may be income tax benefits to diversifying not only your investments, but also your contributions across tax-exempt, tax-deferred, and taxable accounts.

- For your current scenario, we assume you do not monitor the balances in your tax-exempt, tax-deferred, and taxable accounts to ensure each has a minimum percentage in your retirement portfolio.

- For the ComposedPro scenario, we first ensure you are contributing the minimum amount to get the max employer match (if applicable), and then we direct contributions to your tax-exempt, tax-deferred, and taxable portions of your portfolio as to attempt to get them to a minimum percentage of your portfolio. For example, suppose our internal minimum is for each to comprise at least 20% of your overall portfolio and your current balances are 10% tax-exempt, 60% tax-deferred, and 30% taxable. In this case, we would contribute enough to ensure you received your max employer match, and then direct your remaining contributions to tax-exempt accounts since the 10% balance you currently have is less than our desired minimum of 20%.

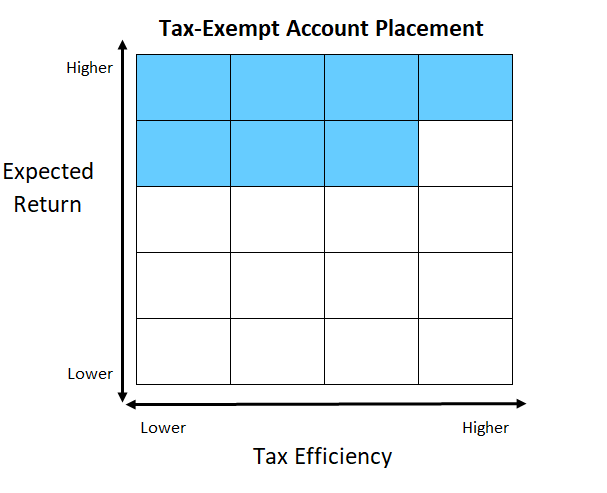

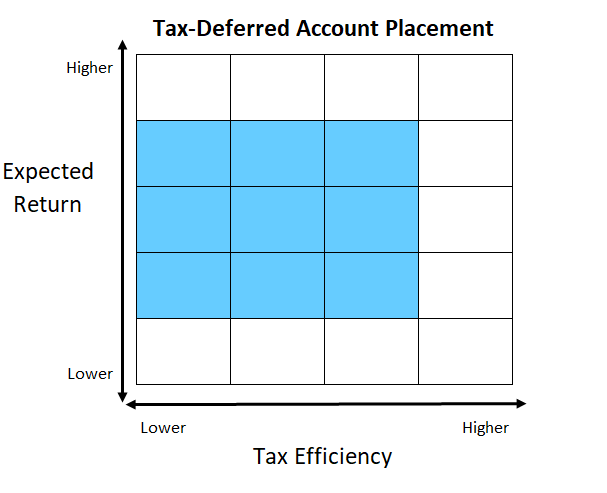

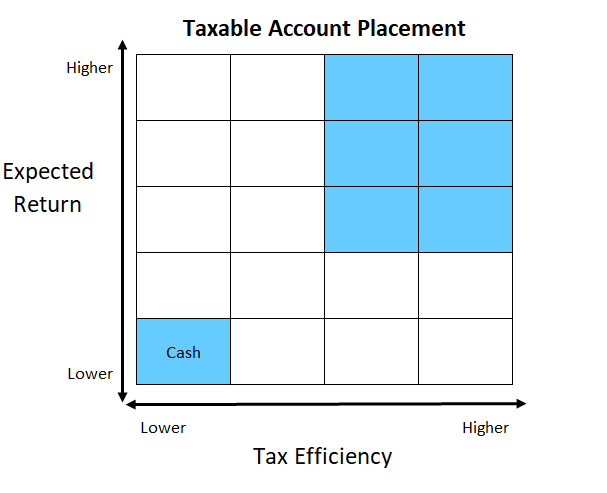

5. Asset Location Savings - these are income tax savings you may realize by smartly placing investments among tax-exempt, tax-deferred, and taxable accounts.

- For your current scenario, we assume you pay little attention to asset location and essentially invest each account in a target-date fund. That is to say - you put all investment asset categories in each of your accounts and do not properly place them across your tax-exempt, tax-deferred, and taxable accounts. For example, your tax-exempt accounts will contain investments in all asset categories: US equities, Non-US equities, US bonds, Non-US bonds, etc. The same with your tax-deferred and taxable accounts. Some of these investments would be better placed in the accounts where they belong.

- For the ComposedPro scenario, we assume a more detailed approach to asset location. You can take a deeper dive into ComposedPro's Investment Methodology, but we generally place investments according to the framework below:

Tax-exempt accounts - place investments with the highest expected return or a high expected return that are also tax-inefficient. Investments could include Non-US Emerging Market Equities or US High Yield Bonds.

Tax-deferred accounts - place investments with a medium-to-high expected return that are also tax-inefficient. Investments could include US Corporate Bonds or Non-US Developed Bonds.

Taxable accounts - place investments with a higher expected return that are also tax-efficient and always tax-exempt bonds. Investments could include US Large Cap Equities or US Municipal Bonds. Any cash in the portfolio is also attempted to be held in taxable accounts because we prefer tax-advantaged accounts to be fully invested.

Please see our discussion on Asset Categories to see how ComposedPro tries to place each within your portfolio.

Smart investment placement through the framework above allows us to create an Asset Location Heat Map™ and a Smart Location Percentage™.

The assumptions described above that are used in the Savings Quiz may not be accurate for your unique situation. The results of the savings quiz are for informational purposes only. The projected savings or other information generated by the Savings Quiz will not match actual results and are not a guarantee of any current or future savings.

Disclosures:

Please note that higher tax-deferred balances could result in higher required minimum distributions (RMDs) in retirement. This should be considered when implementing any contribution recommendations or other such strategies that seek to optimize across tax-exempt, tax-deferred, or taxable accounts. If you are seeking to minimize RMDs, a contribution strategy that recommends a higher tax-deferred balance in your portfolio may not be appropriate. Please consult your tax advisor when implementing any strategy that attempts to lower income taxes.

Clients may not realize the benefits of asset location or other strategies discussed herein. Factors that affect an asset location strategy include, but are not limited to, market performance, the relative size of each account included in financial plan, the equity exposure of the portfolio, the frequency and size of deposits into the various accounts, the tax rates applicable to the investor in a given tax year and in future years, and the time elapsed before the liquidation of any of the accounts becomes necessary.

Nothing herein should be interpreted as tax advice. ComposedPro does not represent in any manner that the tax consequences described herein will be obtained or result in any particular tax consequence. Please consult your personal tax advisor as to whether ComposedPro's asset location strategy is a suitable strategy for you, given your particular circumstances. The tax consequences of an asset location strategy are complex and uncertain. You and your tax advisor are responsible for how transactions conducted in your account are reported to the IRS on your personal tax return. ComposedPro assumes no responsibility for the tax consequences to any client of any transaction.

Comments

0 comments

Article is closed for comments.