The following factors should be considered before deciding to rollover a 401(k) or other Employer Account to an IRA. It is ultimately the client's responsibility to determine whether the rollover is beneficial considering the client's circumstances.

Fees and expenses and available investment options

One factor to consider before rolling over an employer account to an IRA is the number of GOOD investment options within the employer account. For example, ComposedPro classifies an investment option as GOOD by considering the following:

- Low Fees - we set fee hurdles that each investment option must satisfy in order to be classified as having low fees. Some asset categories are more expensive to invest in than others so we assign different hurdles that each investment must satisfy. For example, investing in US Large Cap Equities is typically less expensive than investing in Non-US Emerging Equities. So a US Large Cap investment option with a 0.15% expense ratio may not qualify as low-fee, whereas an investment option in Non-US Emerging Equities with the same 0.15% expense ratio may qualify as low-fee.

- Performance as Expected - we next make sure the investment option being analyzed is highly correlated to its benchmark. We determine each investment option's beta and r-squared to assess whether it performs as expected. Beta tells us how much an investment option's price may move in relation to a movement by its benchmark. We require each investment option to have a beta between 0.9 and 1.1. This means that a price change in the benchmark should translate to a similar price change in the investment option. R-squared tells us the percentage of an investment option's movements that are explained by movements in its benchmark. In other words, it tells us the reliability of our beta calculation.

Level of service available

Do you have access to a CFP® or other professional? Does your employer account offer financial planning or other services? Rolling to an IRA may offer you more service than available in your employer account.

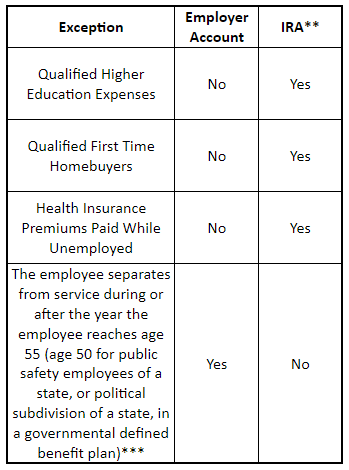

Ability to take penalty-free withdrawals

Normally, if you withdraw from a tax-advantaged employer account (please see special note on 457(b) accounts)* or IRA before the age of 59 1/2 you would be subject to a 10% penalty imposed by the IRS in addition to any income tax imposed on the withdrawal. However, there are certain exceptions from such penalties, and those can differ in an employer account vs an IRA. Below is a summary of exceptions available for employer accounts and IRAs. Please note there are other exceptions available - this only lists the differences in exceptions.

*Please note that 457(b) accounts are not subject to any early withdrawal penalties, and this should be of particular concern when rolling such an account to an IRA.

**SIMPLE IRA distributions incur a 25% additional tax instead of 10% if made within the first 2 years of participation

***Qualified public safety employees - effective for distributions after December 31, 2015, the exception for public safety employees who are age 50 or over is expanded to include specified federal law enforcement officers, customs and border protection officers, federal firefighters and air traffic controllers. Also, the restriction that only defined benefit plans qualify for the exemption is eliminated. Thus, an exemption is allowed for distributions from defined contribution plans or other types of governmental plans, such as the TSP.

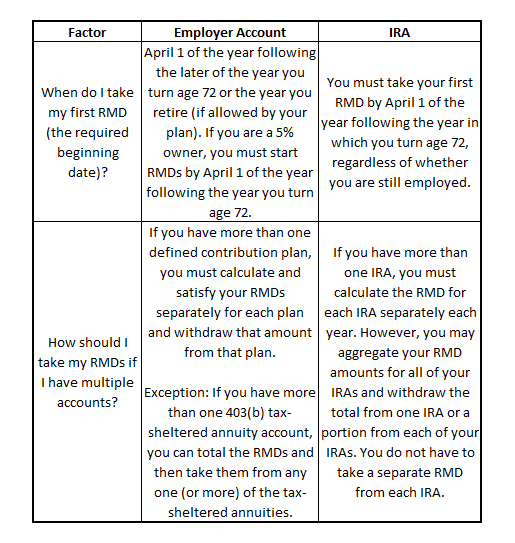

Application of required minimum distributions

Below is a summary of differences in the Required Minimum Distributions from employer accounts and IRAs:

Depending on the state you live in, your IRA may, or may not, be protected from creditors. Some states shield IRAs in nearly all instances, for example, while others offer only limited protection. If you are at risk of creditors pursuing you, speak to a local attorney who understands the nuances of your state. The laws can be complex and you should consult your attorney in regards to this issue as well as your tax advisor as well before making any rollover decision.

Holdings of employer stock

You could have some income tax benefits if you roll over employer stock with unrealized gains held in an employer account to an IRA. Please consult with your tax advisor for further information.

Any special features of the existing account

Your employer account may offer features not available in an IRA, such as the ability to take out a loan. You would not have the ability to take out a loan from an IRA, and other special features offered by the employer account may not be available in the IRA as well.

Disclosures:

The factors to consider before rolling over an employer account to an IRA vary according to your personal situation and preferences. The decision to roll over an employer account may be irrevocable (or very costly to reverse), may involve a substantial portion of your net worth, and can thus have significant long-term impacts. You should consult with your tax advisor before making such a decision.

Comments

0 comments

Article is closed for comments.