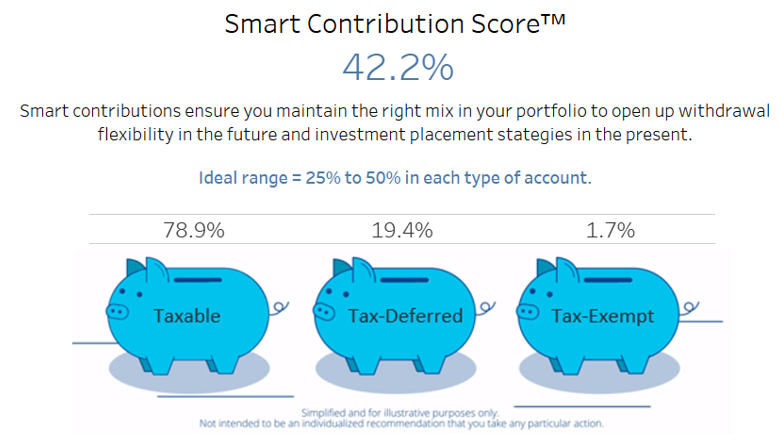

Being diversified amongst tax-exempt, tax-deferred, and taxable accounts may be beneficial due to the flexibility it provides. Nobody knows how income tax rates will look in the future, so a good strategy may be to have more options once the future arrives. Improving your Smart Contribution Score™ means having more options available to you, and more options may give you opportunities to save on income taxes.

Below are two ways contribution diversification may benefit your portfolio:

More Withdrawal Options in Retirement - if you have read our article on retirement withdrawal order, you know there may be some 'abnormal withdrawal years' in retirement at which time you can manage your withdrawals in an attempt to lower your income taxes. Having more options when such a time arises is better than having fewer options should an 'abnormal withdrawal year' present itself. Consider the following two scenarios:

Imagine you are age 65 and retired, and you only have tax-deferred accounts. Any time you make a withdrawal from a tax-deferred account, you would pay high ordinary income tax rates on the full amount of the withdrawal. Perhaps you need more money in a particular year than you normally would because of traveling or medical needs. A higher withdrawal that year could push you into a higher income tax bracket and cost you more in taxes. If you had tax-exempt or taxable accounts at your disposal, you would have more options at your disposal.

The reverse is also true. Imagine you are age 65 and retired, and you only have tax-exempt accounts. For whatever reason, in a particular year, you need to withdraw less from your accounts than in a normal year. This could pull you into a lower income tax bracket that year. If you had only tax-exempt accounts, you might not benefit from being in the lower income tax bracket. If you had a tax-deferred account at your disposal, you might be able to take advantage of a year where your withdrawal needs are abnormally low.

Better Asset Location Opportunities - maintaining the proper balances across tax-exempt, tax-deferred, and taxable accounts may allow you to increase the benefits of an asset location strategy. You could increase your Smart Location Score™, which may allow you to save more on income taxes. Certain investments may be better placed in specific types of accounts. At the most generic level, taxable bonds might be poorly placed in taxable accounts because they throw off interest income that would be taxable each year. Taxable bonds could be better placed in a tax-deferred account to avoid income tax today. Maintaining the proper balances across tax-exempt, tax-deferred, and taxable accounts may open up more asset location opportunities and may improve your outcome.

Disclosures:

Please note that higher tax-deferred balances could result in higher required minimum distributions (RMDs) in retirement. This should be considered when implementing any contribution recommendations or other such strategies that seek to optimize across tax-exempt, tax-deferred, or taxable accounts. If you are seeking to minimize RMDs, a contribution strategy that recommends a higher tax-deferred balance in your portfolio may not be appropriate. Please consult your tax advisor when implementing any strategy that attempts to lower income taxes.

Clients may not realize the benefits of asset location or other strategies discussed herein. Factors that affect an asset location strategy include, but are not limited to, market performance, the relative size of each account included in the financial plan, the equity exposure of the portfolio, the frequency and size of deposits into the various accounts, the tax rates applicable to the investor in a given tax year and in future years, and the time elapsed before the liquidation of any of the accounts becomes necessary.

Nothing herein should be interpreted as tax advice. ComposedPro does not represent in any manner that the tax consequences described herein will be obtained or result in any particular tax consequence. Please consult your personal tax advisor as to whether ComposedPro's asset location strategy is a suitable strategy for you, given your particular circumstances. The tax consequences of asset location are complex and uncertain. You and your tax advisor are responsible for how transactions conducted in your account are reported to the IRS on your personal tax return. ComposedPro assumes no responsibility for the tax consequences to any client of any transaction.

Comments

0 comments

Article is closed for comments.